A bubble in pessimism

It is the combined productive capacity of China’s workers, capital and know-how that sets a maximum speed for the economy, determining how fast it can grow without inflation. It also decides how fast it must grow to avoid spare capacity and a rise in the numbers without work. The latest figures suggest that the sustainable rate of growth is closer to China’s current pace of 7.5% than to the 10% rate the economy was sizzling along at.

For many economists, this structural slowdown is inevitable and welcome. It marks an evolution in China’s growth model, as it narrows the technological gap with leading economies and shifts more of its resources into services. For Mr Krugman, by contrast, the slowdown threatens China’s growth model with extinction.

China, he argues, has run out of “surplus peasants”. Chinese flooding from the countryside into the factories and cities have in the past kept wages low and returns on investment high. The flood has slowed and, in some cases, reversed. So China can no longer grow simply by allocating capital to the new labour arriving from the fields. “Capital widening” must now give way to “capital deepening” (adding more capital to each individual worker). As it does so, investment will suffer “sharply diminishing returns” and “drop drastically”. And since investment is such a big source of demand—accounting for almost half of it—such a drop will be impossible to offset. China will, in effect, hit a “Great Wall”. (The metaphor is so obvious you can see it from space.)

The question is whether Mr Krugman’s concerns are justified. He is right about China running out of “surplus” labour. China’s countryside is no longer so overmanned that people can leave without being missed. Now when they go, the job market tightens and wages rise in the places they leave behind. To tempt them away, wages must rise in the places to which they go.

Yet Cai Fang of China’s Academy of Social Sciences believes that China ran out of surplus countryside labour as far back as 2003. If the economy were going to run into a wall, it would have done so a decade ago. In fact, the economy has since enjoyed spectacular growth. For some time, the movement of workers from agriculture into industry and services has not been the chief source of China’s success. From 1995 to 2012 this movement added only 1.4 percentage points to China’s annual growth, says Louis Kuijs of the Royal Bank of Scotland. Instead, most recent growth has come from raising the productivity of workers within industry, not moving new ones in. Mr Krugman fears the extinction of a model China is already doing without.

He and other respected commentators, notably Michael Pettis of Peking University, are certainly right to criticise China’s high investment rate, for it is a source of great inefficiency. Investment should expand an economy’s capacity to meet the needs of its consumers or its export markets. But in China, Mr Krugman argues, much investment spending is Sisyphean: it is simply adding to the economy’s capacity to expand its capacity.

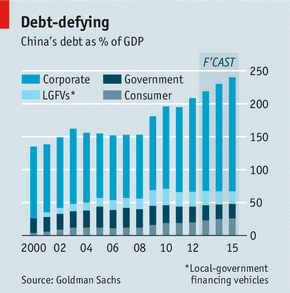

Yet over-investment is not yet a source of instability, thanks to a system that depends on captive savers. Because the government sets an interest-rate ceiling on deposits, the banks underpay depositors and undercharge corporate borrowers—in effect, a tax on household savers and a subsidy for state business. According to a 2012 paper by Il Houng Lee of the IMF and co-authors, this transfer from households to big borrowers averaged an annual 4% of GDP in 2001-11. The subsidy allows big firms to invest in projects that would otherwise be unviable. The authors reckon China’s investment rate should be closer to 40% than 48%. But the distortion can be sustained while depositors continue to finance it—and, given also China’s controls on capital outflows, they have little choice.

It is clear that China should lower its investment rate. But Mr Krugman and others say that a lower investment rate could precipitate a crash. Their concern echoes a 70-year-old model of growth devised by Roy Harrod and Evsey Domar, in which the economy is balanced on a knife-edge between boom and bust.

The model recognises that investment plays a dual role in an economy. It is, as Martin Wolf of the Financial Times puts it, both “a source of extra capacity” and a “source of demand”. Sometimes these two roles work at cross purposes. If growth slows, then the economy will not need to add as much capacity. That implies less investment. But because investment spending is a source of demand, less of it also implies less demand, lowering growth still further. In avoiding excess capacity, the economy ends up creating more of it.

But how well does this model fit China? The country has both one of the world’s highest investment rates and one of its most stable growth rates. That is presumably because investment is partly orchestrated by the government, which encourages more capital spending when other sources of demand are weak, and vice versa. China’s state-owned enterprises and local-government investment vehicles may not allocate capital to the right things. But at least they mobilise it at the right moments.

Indeed, the inefficiency of Chinese investment may be one reason why it will not create great instability. Mr Lee and co-authors point out that China now requires ever higher investment to generate the same rate of growth (its incremental capital-output ratio, as economists call it, is rising). But a corollary is that the same rate of investment is consistent with China’s slowing rate of growth.

Pessimists worry that slower growth will require less investment in capacity, which will, in turn, depress demand. But if the reason for slower growth is a reduction in the efficiency of investment, then slower growth will require just as much of it, precisely because it delivers less bang for the buck.

The fat pipes of the financial system

A similar credit boom preceded America’s crisis in 2008, and Japan’s

in the early 1990s. It is therefore natural to fear that China will

suffer a similar fate. But a closer examination of their experience

suggests that China is unlikely to repeat it.Economists sometimes divide America’s woes into two phases: first the housing bust and then the Lehman shock. America’s house prices began falling as early as 2006, damaging household wealth. Housebuilding slowed sharply, weighing on growth, and many construction jobs disappeared. But for two years America’s central bank, the Federal Reserve, was able to offset much of the harm to growth, while unemployment rose only modestly.

All that changed in September 2008 when Lehman Brothers went bust, triggering acute financial panic. Nobody knew how big the losses from mortgage defaults might be, nor who might end up having to bear them. Creditors, shareholders, marketmakers and traders all rushed to make sure it was not them, by pulling credit lines, demanding collateral and dumping their securities.

In many ways, their dash for the exits proved to be more damaging for the economy as a whole than the danger from which they were seeking to escape. After the Lehman shock, a manageable number of mortgage insolvencies became a catastrophic liquidity problem. The lending mistakes of the past crippled the supply of finance in the present.

Some economists argue that efforts to sustain demand will prove misguided. An unsustainable boom will leave workers stranded in the wrong jobs, making a painful bust necessary to reallocate them. Yet restructuring is not unique to a recession. Even in a steadily growing economy, plenty of upheaval is going on under the surface, as people are hired and fired, and as they hop between jobs of their own volition. Just as busts push workers out of declining industries and into unemployment, so booms pull them out of sunset industries into sunrise ones.

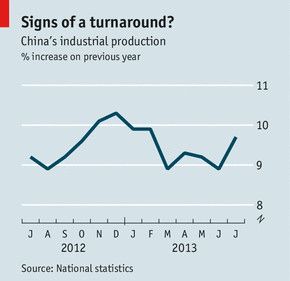

China is no stranger to economic restructuring. Over the past decade, the share of workers in agriculture fell from half to about a third. Exports have fallen from 38% of GDP in 2007 to 26% last year, while services now contribute as much to the economy as industry. And this enormous shake-up of employment and production took place in an economy that was growing by about 10% a year. China’s economy can, it seems, evolve and expand at the same time.

No comments:

Post a Comment